how to get an exact injection molding cost sheet

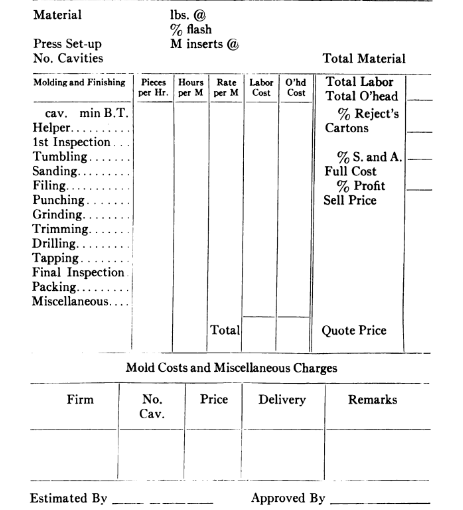

There are innumerable different styles of estimate sheets. Some include information regarding the estimated figures only, while others are used to record facts pertaining to production and actual cost comparisons. Figure 1 exemplifies a concise form of standard estimate sheet which is applicable to any item where it is required to prepare selling prices for the customer.

Figure 1

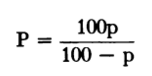

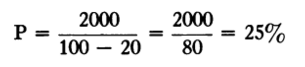

It will be noted that provision is made for overhead cost after each operation inasmuch as sometimes this quantity is a variable and, therefore, appears as a different percentage on the corresponding labor cost. After we arrive at the primeplastic molding companies cost we then apply the sales and administrative estimated values. Finally, the percentage of profit is added to the total to obtain the selling price. It should be remembered, however, that net profit is based on selling price and that the amount used to obtain the selling price is not actually the amount of net profit realized. In other words, if the full factory cost amounted to $80.00 per thousand and to this was added 25% for profit the selling price would then be $100.00 but the net profit in such a case is not 25% but 20%. The actual net profit is the percentage ratio of the difference between the full plastic molding companies cost and the selling price. If it is desired to find the correct percentage to apply to a full plastic molding companies cost in order to obtain a given net profit on the selling price this can be accomplished by merely substituting in the following formula:

P is the unknown percentage which should be applied to the full plastic molding companies cost in order to get the desired profit wanted in percentage. The percentage of profit wanted is designated by p. Thus if it is desired to get a 20% net profit on an item which has a full plastic moulding supply factory of any value whatsoever we can see that it must have 25% added to it.

This will apply to any value and is therefore helpful in assuring that the real net profit based on selling price will be obtained.

Now that we have studied the estimate form and thoroughly understand it let us work out a problem utilizing this knowledge.

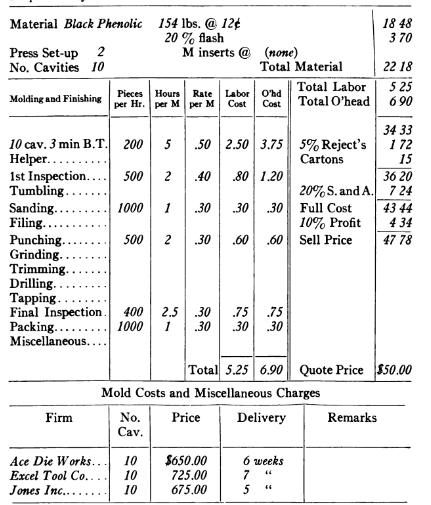

Let us say, for instance, that a customer submits a blue print showing a piece rectangular in shape, about 4f/ X 2″ X 1〃 deep. It has two holes in the base that have to be punched out and he asks for a custom plastic piece price based on quantities of fifty thousand lots. He stipulates that he would like to have figures furnished on a ten cavity mold, the piece to be made of black phenolic material. At the outset we take off quantities from the print and find that the part would have an approximate weight of 154 pounds per thousand. This is, of course, net weight so we have to add a certain percentage in order to get the gross. Let us now look at Figure 2. Here is the estimate form made out on the basis of the information submitted. We can follow this through from the beginning and see how the ultimate selling price was obtained.

In the first place the material price is found to be twelve cents a pound and inasmuch as no provision is made for tabletting in the estimate the powder price must include this preparation cost. Some firms prefer to set up a separate operation for pilling, but inasmuch as it is labor performed on material prior to its function in the molding process it is commonly included in the material cost per pound. After finding the net material cost, 20% is then added for flash or overflow to give the gross material figure. We turn next to the molding operation. In deciding the pressing cost the cycle time is usually used for a basis, so in this instance three minutes was presumed to be sufficient. If it takes three minutes to complete one heat we know that twenty heats should be ejected in an hour, and if we multiply the number of heats by the mold capacity we then obtain the total hourly production. In this case we have a ten cavity die and therefore two hundred units should be produced in an hour. Converting this into the number of hours required to make a thousand and multiplying by the prevailing labor amounts to $2.50 and the overhead is then obtained by taking a percentage of the labor. In the example given, overhead has been assumed to be 150% in the press room and 100% in the finishing room, this accounts for the values given in the overhead column. The method of arriving at overhead percentages will be dealt with in detail later. For the present at least is suffice to note that the total labor and overhead is added to the material cost, after which is appended the rejection and carton price figures to obtain the prime factory cost. In looking back at the finishing operations we find that the piece was charged with first and final inspection, sanding, punching, and, of course, packing.

In the first place the material price is found to be twelve cents a pound and inasmuch as no provision is made for tabletting in the estimate the powder price must include this preparation cost. Some firms prefer to set up a separate operation for pilling, but inasmuch as it is labor performed on material prior to its function in the molding process it is commonly included in the material cost per pound. After finding the net material cost, 20% is then added for flash or overflow to give the gross material figure. We turn next to the molding operation. In deciding the pressing cost the cycle time is usually used for a basis, so in this instance three minutes was presumed to be sufficient. If it takes three minutes to complete one heat we know that twenty heats should be ejected in an hour, and if we multiply the number of heats by the mold capacity we then obtain the total hourly production. In this case we have a ten cavity die and therefore two hundred units should be produced in an hour. Converting this into the number of hours required to make a thousand and multiplying by the prevailing labor amounts to $2.50 and the overhead is then obtained by taking a percentage of the labor. In the example given, overhead has been assumed to be 150% in the press room and 100% in the finishing room, this accounts for the values given in the overhead column. The method of arriving at overhead percentages will be dealt with in detail later. For the present at least is suffice to note that the total labor and overhead is added to the material cost, after which is appended the rejection and carton price figures to obtain the prime factory cost. In looking back at the finishing operations we find that the piece was charged with first and final inspection, sanding, punching, and, of course, packing.

to be continued…